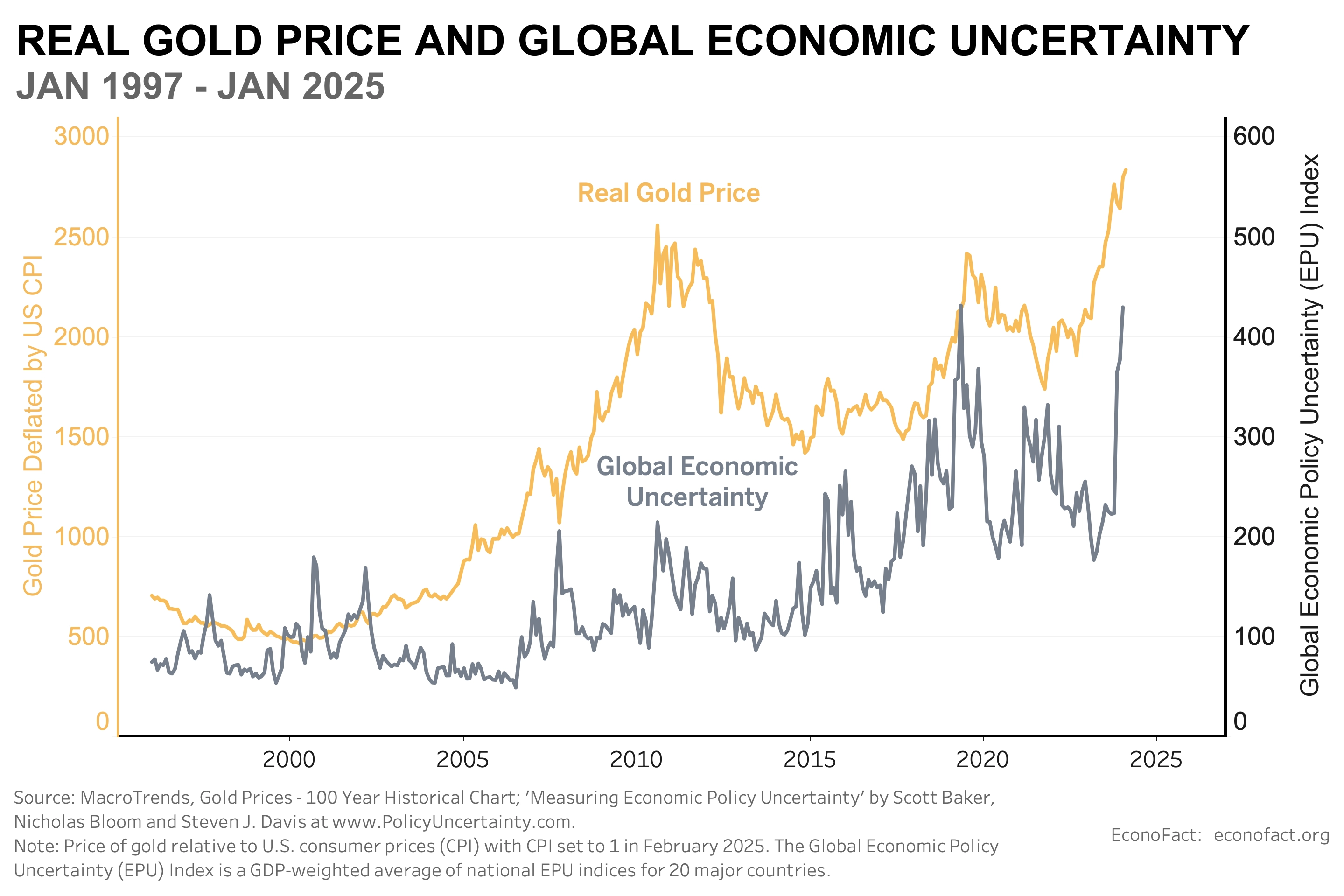

Gold as a Safe Haven

It is widely known that gold survives when national systems collapse. Its supply barely grows — money can be printed by central banks, but gold doesn't suddenly appear from the ground. So as the value of currency falls, gold's relative value rises. Wars often bring inflation, and gold tends to move with it. It's also a physical asset that crosses borders.

Compared to other assets: stocks are worthless if the company goes bankrupt, bonds fail if the government collapses, but gold holds its value wherever you take it. So the conventional wisdom is: war breaks out → gold goes up.

Source: Econofact

The chart shows a clear correlation — as geopolitical and policy-driven uncertainty rises, gold follows.

What Happened in the US-Iran War?

| Date | Event |

|---|---|

| Jun 13–24, 2025 | The Twelve-Day War |

| Jan 2026 | Iran's largest protests since 1979 |

| Feb 6, 2026 | Muscat nuclear talks (Round 1) |

| Feb 28, 2026 06:35 UTC | Operation Epic Fury begins |

| Feb 28, 2026 06:45 UTC | Supreme Leader Khamenei assassinated |

| Feb 28, 2026 09:05 UTC | Iran fires missiles at US bases and Israel |

| Mar 1, 2026 | Mojtaba Khamenei becomes Supreme Leader |

| Mar 4–18, 2026 | Hormuz closed — Qatar's Ras Laffan struck |

| Apr 5–6, 2026 | Islamabad talks collapse |

| Apr 13, 2026 | US Navy blockades Iranian ports |

Gold showed a consistent downward trend from Feb 22 through late March.

GC=F, Feb 18 – Apr 13

Geopolitical risks rise in late February:

So Why Did Gold Fall?

This war didn't follow the usual "uncertainty → buy gold" path. Instead it went: oil price spike → inflation reignited → Fed rate cut expectations destroyed → dollar strength → gold selloff.

Gold rises when rate cuts are expected, because it pays no interest. When the Hormuz closure sent oil prices surging, markets concluded the Fed would keep rates higher for longer — and the case for holding gold evaporated. Dollar strength compounded this. Since oil is priced in dollars, rising oil prices created real physical dollar demand from governments, refiners, and energy companies all at once, pushing DXY higher. With dollar assets like T-bills and MMFs yielding more, there was simply no reason to hold non-yielding gold. On top of that, as dollar strength increased the burden of dollar-denominated debt globally, risk-off sentiment deepened, reducing gold's appeal further and triggering some forced liquidations.

The bottom line: the character of war matters. Energy-linked Middle East conflicts are bad for gold. They push rates up and the dollar higher. By contrast, a scenario where the dollar system itself is threatened — like the 2008 subprime crisis — is far more favorable for gold.

US Dollar Index (DXY)

When Gold Fell, Where Did the Market Go?

| Asset | Direction | Interpretation |

|---|---|---|

| GC=F (Gold) | ↓ | Safe haven function failed |

| DXY | ↑ | Oil settlement demand + risk-off |

| TLT (Long-term bonds) | ↓ | Bond selloff on inflation fears |

| JPY | ↑ | Traditional safe haven working |

| CHF | ↑ | Traditional safe haven working |

| CL=F (Oil) | ↑↑ | Direct reflection of Hormuz closure |

In this war, the safe haven wasn't gold — it was the dollar. The fact that TLT also sold off tells you the market read this as an inflation shock, not a geopolitical uncertainty event.

Key Takeaways

The "war = buy gold" formula doesn't always apply. It depends on the nature of the conflict. What's needed is a multi-factor regime classifier that looks at three variables simultaneously: DXY direction × real interest rate direction × degree of prior shock pricing-in.

Simple Framework for Gold's Safe Haven Regime

The core idea is that gold doesn't respond to war itself — it responds to the macro environment the war creates. Three variables determine which regime you're in:

1. DXY Direction

Is the dollar strengthening or weakening? A stronger dollar directly suppresses gold and signals that capital is fleeing to dollar assets, not gold.

2. Real Interest Rate Direction

Are real yields rising or falling? Rising real rates increase the opportunity cost of holding non-yielding gold. When the market believes a war will reignite inflation and keep the Fed on hold, real rates stay elevated — and gold struggles.

3. Degree of Prior Shock Pricing-In

Was this war a surprise, or did markets see it coming? A fully anticipated conflict means the fear premium is already in the price before the first shot is fired. When the event actually happens, there's nothing left to buy — it's a classic buy the rumor, sell the news dynamic.

How the Regimes Play Out

| DXY | Real Rates | Surprise Factor | Gold Regime |

|---|---|---|---|

| ↓ | ↓ | High | Strong buy — classic safe haven |

| ↑ | ↑ | Low | Sell — this war, exactly |

| ↓ | ↑ | High | Weak buy — mixed signals |

| ↑ | ↓ | Low | Neutral — dollar vs. rate cut tug of war |